As Apartments Boom And Middle Housing Lags, The South Emerges As The Fastest-Growing Housing Region

Key takeaways:

- The national housing inventory rose by 16.7% from 2005 to 2023.

- The multifamily sector saw the most rapid growth, increasing by 54% nationwide. Apartment stock doubled or more in over 120 cities.

- Middle housing grew by just 11.3%, while single family homes increased by 16.7% during the same period.

- The South leads in housing inventory expansion, with over 30 of the top 50 cities for growth in the region — nearly half of which are in Texas.

- The Dallas-Fort Worth Metroplex races ahead in housing stock expansion, with Frisco emerging as the fastest-growing housing market in the U.S.

- Cities in the Midwest saw the most significant reductions in housing stock.

- Although 91% of U.S. cities saw inventory increases, home prices rose in 99.4% of cities from 2005 to 2023.

The U.S. housing market has been on a steady, albeit slow, growth trajectory over the past two decades. Total inventory reached 144 million housing units in 2023, a 16.7% increase from 2005, according to the latest U.S. Census data. But while homes continue to be built, housing supply still falls short of meeting demand, and prices keep rising. Freddie Mac estimates a current deficit of approximately 3.7 million homes that would be needed to bring vacancy rates back to historical norms.

Inventory growth over the past two decades has been anything but smooth. The economic downturn and health crisis both sent shockwaves through the housing market. While the 2010s were defined by recovery from the Great Recession, 2022 and 2023 saw a rebound, bringing construction levels back to those of 2006 and 2007, with a more typical annual increase of over 1%.

The housing stock evolved differently across various housing types, with single family and middle housing underperforming while multifamily developments boomed.

Single family homes, often slower and more costly to build, couldn’t keep up with demand, especially in high-growth areas. Overall, from 2005 to 2023, single family housing stock increased by a modest 16.7%, bringing the total inventory to nearly 89 million units.

The less-than-ideal evolution of the single family housing market was largely due to the effects of the economic downturn, which left the sector grappling with high construction material costs, labor shortages, lending challenges and restrictive zoning regulations — all contributing to a slower pace of construction. For much of the period between 2005 and 2023, annual expansions remained below 1%.

Middle housing — generally defined as a class of housing types including structures such as duplexes, triplexes, condos, townhomes, cluster homes, cottage courts and live/work units — has often been touted as a potential solution to the affordability crisis. However, it has yet to gain significant momentum. It has seen an underwhelming 11.3% expansion from 2005 to 2023, the lowest inventory increase among the major housing types. However, there is a silver lining: 2022 saw an accelerated growth rate of 1.6% year-over-year, largely driven by state-level initiatives aimed at easing the housing crunch. California has been particularly active, passing a series of laws since 2017 to support housing development, including middle housing. Other cities, such as Portland, Minneapolis, Washington, D.C., and Buffalo, have followed suit. Beyond affordability, middle housing — such as condos, townhouses, duplexes and triplexes — offers additional benefits. These housing types are ideal for multigenerational living, allowing families to live close by while maintaining separate homes, and they also help foster a sense of community. Of the 145 million total housing units in the U.S., 33 million fall into the middle housing category.

Amid the sluggish growth in single family and middle housing, the multifamily sector stepped up to meet the pressing need for more living space. From 2005 to 2023, multifamily housing boomed, with stock increasing by 54% to over 15 million apartment units by 2023 — a golden age for the sector. Multifamily had a particularly good performance in 2022, when stock went up 5% year-over-over. Similarly, in 2023, apartment inventory grew 3% nationally.

Other housing types, including manufactured homes, RVs, vans and other nonconventional structures used as primary residences, have also seen notable expansion. Overall, these housing options have nearly doubled in number since 2005, although they still represent a small fraction of the total housing inventory.

The steady housing stock expansion has spilled over into the self storage sector, adding momentum to an industry that once flew under the radar. The 2020s are turning out to be the biggest decade yet for self storage construction. Right now, we’re seeing over 64 million square feet of new space added each year, beating the almost 56 million square feet peak we hit back in the 2000s.

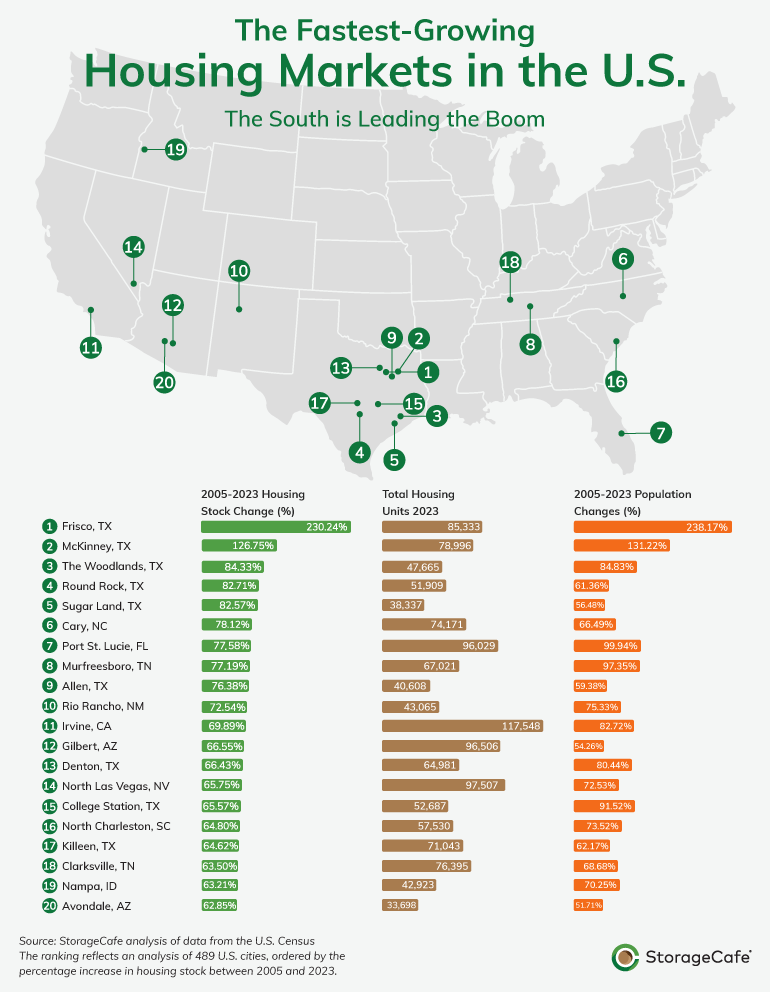

America's boomtowns: Cities with the fastest growth in housing inventories

With self storage closely linked to household formation and housing development, our research team at StorageCafe set out to pinpoint the cities leading efforts to ease the national housing shortage. We analyzed 489 cities with populations over 55,000, ranking them based on local inventory growth across various residence types — including single family, multifamily, middle housing, mobile homes, boats, RVs and vans. To assess the broader impact of housing growth, we incorporated additional data on housing availability (units per capita), pricing and employment. Since self storage supports both homeowners and renters in optimizing their living spaces, we also examined this sector to monitor inventory changes and their relationship with residential development.

Regionally, the South leads, with 31 cities among the top 50 for overall housing inventory growth between 2005 and 2023, nearly half of which are in Texas. As an economic powerhouse, the South has drawn newcomers primarily to Florida, Texas and North Carolina, three of the most popular states for relocation. This accelerated migration has fueled robust construction efforts to meet the surging housing demand.

In the West, 18 cities also saw substantial increases in residential inventories. Sioux Falls, SD, stands as the only Northeastern city among the top 50 cities for housing growth during this period, highlighting the region’s comparatively slower expansion.

The South leads U.S. housing stock growth from 2005 to 2023, with Texas cities stealing the spotlight

Experiencing an economic boom over the past decade and beyond, Texas has become a migration hotspot thanks to its strong job market, business-friendly environment and amenity-rich communities. This influx of newcomers has, in turn, spurred a surge in housing demand, leading to intensified construction activity. As a result, Texas now ranks at the forefront of national housing inventory growth, with 15 cities standing out among the top performers in housing stock increases from 2005 to 2023.

The Dallas metro area stands out for its high density of top-growth housing markets, with Frisco, TX, emerging as the fastest-growing housing market in the country. From 2005 to 2023, Frisco more than tripled its housing inventory, reaching over 85,000 units. In terms of housing types, Frisco ranks first nationally for both multifamily and single family stock increases over this period. The local apartment stock skyrocketed by over 1,200%, totaling more than 17,000 units in 2023, while single family homes rose by 225%, reaching 61,000 units.

As residents often turn to self storage for additional space, the sector has expanded in response. Frisco’s self storage inventory reached approximately 1.7 million square feet in 2023, more than doubling over nearly two decades. The average cost of a storage unit in Frisco is $142 per month.

Also in the Dallas area, McKinney boasts the second-most-significant housing stock expansion, with an increase of 127% from 2005 to 2023, reaching nearly 79,000 units. McKinney also stands out for having the fastest-growing middle housing stock, up 185% over this period. Neighboring Allen, TX, follows closely with an impressive 182% growth in townhouses, condos, duplexes, triplexes and other middle housing types.

Fort Worth, bolstered by the presence of several Fortune 500 companies, saw a 65% rise in job numbers between 2005 and 2023, attracting a wave of newcomers. Consequently, the city’s population grew by 62%, driving demand for housing. To meet this demand, housing units rose by 56%, bringing the total inventory to over 380,000 units in 2023.

In the Houston area, The Woodlands ranks third nationally for housing stock growth, with an 84% increase from 2005 to 2023, bringing its total housing inventory to around 48,000 units. This surge in construction aligns with the area’s expanding population, which also rose by 84% over the same period. Multifamily housing experienced the most rapid growth, soaring 273% to over 6,600 apartment units. Notably, The Woodlands is the only top-performing city to experience a slight decline in middle housing inventory, which decreased by 4% from 2005 to 2023. This decline is largely attributed to the area’s predominant single family zoning and limited land availability in Montgomery County.

North Carolina, Florida and Tennessee solidify the South’s status as the fastest-growing region for housing

Beyond Texas, North Carolina stands out with multiple cities expanding their housing inventories significantly between 2005 and 2023. Cary leads the state with a 78% increase in overall housing inventory, driven by a prolific apartment sector that grew over 200% during this period. Meanwhile, Charlotte saw even more remarkable growth in multifamily housing, with a 245% expansion. Durham also made strides in the apartment sector, more than doubling its inventory by 2023, while Fayetteville contributed to the state’s multifamily boom with a substantial 90% increase in apartment stock.

This growth across North Carolina cities is largely fueled by above-average population increases as newcomers are drawn by the economic and employment opportunities supported by the Raleigh-Durham-Chapel Hill Research Triangle.

Still in the South, several cities in Florida are making waves with impressive housing inventory growth. The Sunshine State has consistently ranked as a top destination for Americans on the move. Among Florida’s best performers in residential supply growth, Port St. Lucie (99%) and Cape Coral (67%) saw substantial population increases between 2005 and 2023. Port St. Lucie led in housing growth, with a 78% increase that brought its total housing units to around 96,000 in 2023. Orlando and Miami also saw notable expansions, with total housing growing by over 40% in each city. Orlando experienced nearly 50% growth, while Miami reached a total of 234,000 units compared to Orlando’s 153,000.

Overview of Miami, FL, with residential buildings at the forefront

Both cities saw significant growth in apartment inventory, with Miami’s multifamily stock rising 157% to 119,000 units and Orlando’s increasing 132% to 38,000 units. Cape Coral, in contrast, had the slowest apartment growth among this group, with a 33% increase by 2023.

Moving inland, Murfreesboro, TN, has become one of the best places to live in the U.S., thanks to its blend of big-city amenities, quality schools, a robust economy and appealing housing options. The city’s population surged by 97% from 2005 to 2023, driving a 77% growth in housing inventory. Multifamily units expanded by an impressive 142%, bringing the apartment unit count to around 6,300. Single family homes remain the most common, with a total of 36,500 units — a 94% jump by 2023.

Southwestern cities, led by New Mexico and Phoenix, step up to the plate with strong residential growth

In the Southwest, cities in New Mexico are making a significant impact with housing stock growth, with Rio Rancho leading the way. Local housing supply rose by 73% from 2005 to 2023, reaching a total of 43,000 units. Mobile homes saw a remarkable 100% increase, driven by the area’s mild climate. Single family homes, which constitute the largest portion of Rio Rancho’s inventory at 38,000 units, grew by 75% over this period.

Other cities in New Mexico — Santa Fe and Las Cruces — experienced similar housing growth, with increases of around 45%. Las Cruces slightly outpaced Santa Fe with about 53,000 housing units in total. Both cities saw population increases of over 34%, supporting steady residential development. In Santa Fe, multifamily housing grew the most, expanding by 115%, while Las Cruces saw a 74% rise in single family homes. The affordability of homes in Las Cruces, with an average price of $246,000 and some of the nation’s lowest property taxes, has made single family homes especially popular.

In neighboring Arizona, cities in the Phoenix area exemplify rapid housing stock growth. Gilbert, Avondale and Surprise have all seen accelerated development, fueled by an expanding business environment and increased job opportunities. From 2005 to 2023, employment increased by over 45% in each city, drawing a substantial influx of new residents. Gilbert led with a 67% increase in housing stock, while Avondale and Surprise followed closely, each growing by over 62%. The multifamily sector experienced exceptional growth in Avondale and Gilbert, expanding by 423% and 374%, respectively. Avondale now has 5,500 apartment units, while Gilbert has a higher count at over 6,600 units. In addition to a larger apartment inventory, Gilbert is known for offering premier rental communities with top-tier amenities.

In Nevada, North Las Vegas and Henderson have attracted Americans seeking new homes in the Las Vegas area. Both cities saw population increases of over 50% from 2005 to 2023, driving growth in the residential sector. North Las Vegas led in housing stock expansion with a 65% increase, although Henderson boasts a higher total with about 147,000 units. Apartments grew fastest in both cities, with Henderson seeing a 296% increase to 12,600 units and North Las Vegas growing by 247% to approximately 3,400 units. Single family homes grew more rapidly in North Las Vegas (60%) compared to Henderson (55%), partly due to more affordable home prices in North Las Vegas at an average of $411,000. Middle housing types also surged, nearly tripling in North Las Vegas with a 70% increase, bringing townhouses, condos and other types of middle housing to over 20,000 units by 2023.

California’s housing growth is driven by tech hubs and college towns

In California, housing inventory growth has been most notable in cities with vibrant tech scenes and student populations. The Golden State claims six of the top 50 cities for residential supply growth. Irvine saw the highest overall housing growth in California with a 70% increase, aligning with an 82% population jump from 2005 to 2023. Irvine’s multifamily sector led the response to housing demand, growing by 185% and bringing apartment units to 32,000 in 2023.

In Indio and Clovis, housing inventories rose at similar rates of 59% and 57%, respectively. Clovis, with a total of 45,000 housing units, has a higher housing supply than Indio, which reached 37,000 units in 2023. Clovis expanded its apartment inventory more, with a 142% increase, while Indio saw an 8% decline in apartment stock. Middle housing supply grew modestly in both cities, at around 3.6% from 2005 to 2023. In Fontana, part of the Inland Empire, housing inventory increased by 48%, with the number of apartments doubling over this period.

Sioux Falls, SD: The Midwest’s housing growth leader

Among the top 50 cities for housing stock expansion, Sioux Falls, SD, is the only representative from the Midwest. The city offers strong employment opportunities in health care, finance and retail, with job growth up 42% since 2005. This has spurred population growth, particularly during the pandemic when Sioux Falls became a popular destination for renters. The city’s population increased by 56% from 2005 to 2023, prompting a nearly 60% expansion in housing stock. Apartments saw remarkable growth, increasing by 114% to over 18,000 units. Although single family homes remain the majority with over 50,000 units, they experienced the slowest growth among the main housing types.

Michigan cities experience the steepest declines in housing inventory

While housing stock increased in most U.S. cities, 56 experienced a decline in residential units. Flint, MI, saw the most significant decrease, with its housing stock dropping by 20% from 2005 to 2023, resulting in a total of 43,000 units. Flint’s well-documented economic decline, largely due to GM downsizing, led to substantial population loss and abandoned properties, which contributed to the reduction in recorded housing inventory.

Detroit, MI — often cited as an emblem of urban decline — followed closely with a 15% decrease in total housing, equating to around 43,000 fewer units between 2005 and 2023. Detroit’s high foreclosure rates and a population decline of about 24% over this period have driven this trend. Interestingly, while both Flint and Detroit saw decreases in single family home counts, apartment numbers actually rose, with Detroit recording a modest 7% increase and Flint seeing about a 22% rise in apartment units.

Housing stock expansion by sector

From 2005 to 2023, the housing stock evolved differently, with the apartment, single family and middle housing each having their own growth trajectory. Let’s take a look at how each sector fared:

Top cities for apartment growth

Apartment supply experienced the sharpest growth among residential sectors, increasing by 54% from 2005 to 2023. In a quarter of the 486 cities analyzed, apartment numbers either doubled or grew at even higher rates. Among the top 50 cities for multifamily inventory growth, over half (31) are in the South, underscoring the region’s housing boom.

Texas cities shine in single family construction

Single family homes remain America’s preferred housing type, and inventory has steadily increased from 2005 to 2023, with Texas leading the way. The Lone Star State claims 12 of the top 50 cities for single family housing growth, largely due to its high migration rates during this period. Several Texas cities saw triple-digit growth in single family homes, with Frisco (225%) and College Station (115%) among the top performers. Other cities, including McKinney (96%), The Woodlands (90%) and Denton (79%), also contributed impressive numbers to the state’s single family housing supply.

Cities making strides to close the “missing middle” housing gap

Though historically more common in urban areas and inner suburbs, “missing middle” housing saw only an 11.3% increase from 2005 to 2023 — the smallest growth among housing types analyzed. However, middle housing reached a substantial 33 million units in 2023, more than double the multifamily stock. Within middle housing, townhouses grew the fastest, increasing by 29% and totaling over 9 million units. As a more affordable option — typically 30% cheaper per unit than single family homes — the rise in townhouses and other middle housing types is a response to demand for diverse and accessible housing options.

Though middle housing experienced slower growth overall, inventories were replenished in 331 cities from 2005 to 2023, with the majority located in the South and West. Leading the charge in Texas, McKinney saw its middle housing stock increase by 185%, while nearby Allen followed closely with an 182% surge. McKinney’s total middle housing inventory reached 17,000 units in 2023, considerably higher than Allen’s 4,300 units. Statewide population growth has supported this expansion, with cities like Odessa seeing a 93% rise in middle housing and Round Rock, Austin and San Angelo each experiencing increases of over 60%.

The West is also well represented, with 22 cities showing notable middle housing growth. Four cities —anchoring major metro areas in California, Arizona and Utah — saw their middle housing inventories double or more. South Gate, CA, led with a 130% increase, while San Marcos, CA (126%), and Gilbert, AZ (125%), expanded at comparable rates. In Utah, Sandy increased its middle housing supply by 109%.

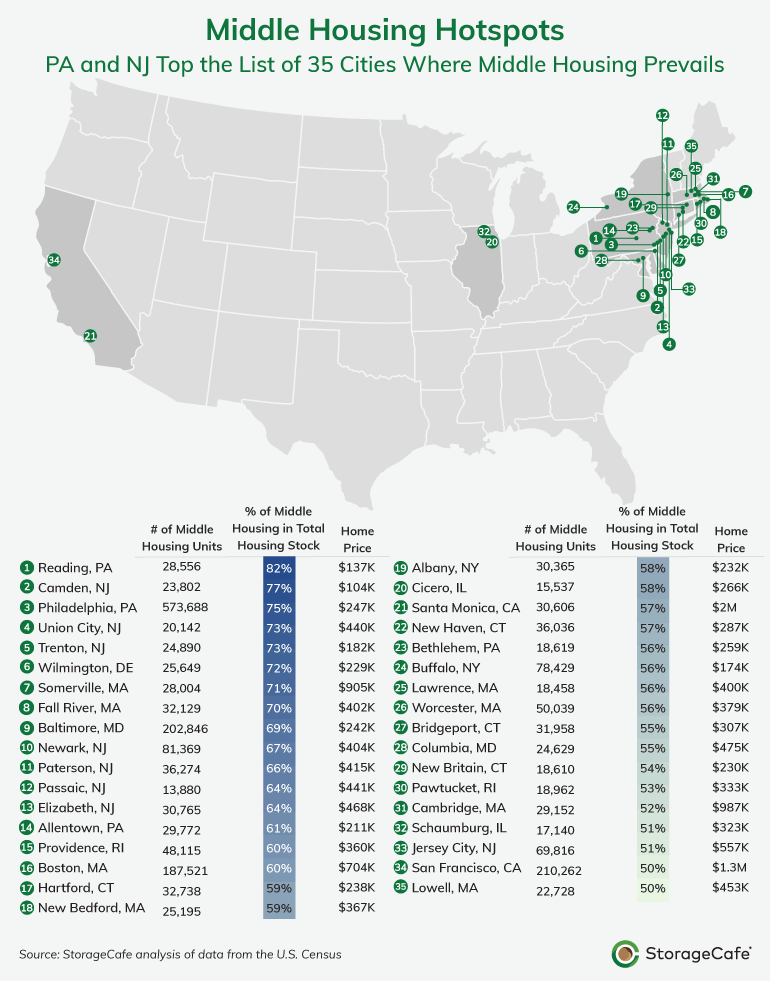

East Coast’s PA and NJ lead the nation in middle housing options

While middle housing is a missing puzzle piece for many cities seeking affordable options, some places are already ahead of the curve, showing how this “missing middle” can help ease the housing crunch. Notably, in about half of the 35 U.S. cities where middle housing makes up the majority of the local market, home prices remain below the national average of $340K—making them a win for affordability.

The East Coast leads in middle housing density, with 30 of the top cities located in this region. In Reading, PA, middle housing comprises an impressive 82% of the 2023 housing stock, with homes priced at an average of just $137K. Philadelphia, with a 75% share of middle housing, also stands out; limited space for expansion makes this type of housing a smart solution for the city’s land constraints. Other PA cities like Allentown (61%) and Bethlehem (56%) follow suit, each with home prices staying below $260K.

In nearby New Jersey, eight cities rank high for middle housing inventory, especially those in the New York metro area, providing affordable alternatives for commuters. Camden (77%) and Trenton (73%) are notable exceptions outside this metro area, with average home prices at $103K and $182K, respectively. Other NJ cities in this area average around $400K, still more affordable than comparable properties in NYC.

The “missing middle” is most pronounced in popular migration hotspots

On the flip side, Arizona and Texas—two of the South’s most popular migration destinations—are struggling with a lack of middle housing. Zoning restrictions and resident pushback have slowed the development of condos, townhouses, duplexes, and other middle housing types, driving up home prices. In cities with limited middle housing, particularly those experiencing high migration rates, home prices are consistently above average.

In Arizona, the Phoenix metro area illustrates the issue perfectly. Gilbert, despite its strong overall housing growth, has the smallest share of middle housing among its neighbors—just 10% of its total housing inventory, or about 10,000 units. Meanwhile, home prices in Gilbert average over $614,000, far above the national average of $340,200 and up a massive 91% over the last two decades. Nearby Phoenix and Chandler offer slightly more middle housing, at 21% of their respective inventories, but prices still soared, with homes averaging over $400,000 in both cities—up 140% and 123%, respectively, since 2005.

Texas has its own challenges. Laredo ranks second nationally for its lack of middle housing, with only 17% of its local inventory (about 15,000 units). Plano and Fort Worth also struggle, with middle housing making up just 20% of their housing stocks. Single family homes dominate in all three cities, and home prices have skyrocketed over the last two decades. In Plano, the average home price sits at $472,500—up 141% since 2005—while Fort Worth has seen an astonishing 213% price increase over the same period.

Adding more middle housing, like duplexes, triplexes, and fourplexes, is increasingly recognized as a practical solution to Texas's affordability crisis. Encouragingly, permits for these housing types have been steadily rising across the state over the past decade, signaling a shift toward more balanced housing options.

Home prices continue to climb despite housing inventory growth

Our report shows that housing inventories increased in 91% of the cities analyzed, yet this growth hasn’t curbed rising home prices. In nearly all cities (99.4%), home prices surged from 2005 to 2023 as supply struggled to keep pace with demand. Similarly, apartment rents rose in every city in our study. Despite the multifamily boom, the sector still fell short of meeting market demand, contributing to the sustained rise in rental prices.

Flint (-17%) and Detroit (-2%) are the only cities where home prices decreased, but both cities also experienced significant inventory losses from 2005 to 2023.

Self storage industry growth mirrors housing expansion

As housing inventory expanded nationwide, so did the self storage industry, which grew by 58% from 2005 to 2023. Self-storage inventory increased across all cities we analyzed, with growth surpassing the national average, primarily in cities that led in single-family housing growth, closely followed by top performers in multifamily inventory expansion.

In Frisco, TX — ranked first for both single family and multifamily inventory growth — self storage space rose by an impressive 141% from 2005 to 2023, reaching 1.6 million square feet, or approximately 3.9 square feet per capita.

Similarly, in College Station, TX, and California’s Clovis and Irvine, self storage inventories doubled or more during this period. Irvine now has over 3.2 million square feet of self storage, while College Station and Clovis each have over 1 million square feet.

Explore the table below to see how self storage availability and pricing compare in some of the largest cities:

Self Storage Growth and Availability Across U.S. Cities (2005–2023)

| Rank | City | % Change in Self Storage Inventory (2005–2023) | Total 2023 Self Storage Inventory (sq. ft.) | Self Storage Per Capita (sq. ft.) |

|---|---|---|---|---|

| 1 | Frisco, TX | 141.32% | 1,677,019 | 3.92 |

| 2 | McKinney, TX | 88.92% | 2,785,220 | 8.32 |

| 3 | The Woodlands, TX | 59.09% | 627,893 | 2.94 |

| 4 | Round Rock, TX | 168.63% | 2,147,573 | 6.67 |

| 5 | Sugar Land, TX | 32.59% | 1,191,152 | 3.26 |

| 6 | Cary, NC | 137.55% | 1,227,140 | 4.69 |

| 7 | Port St. Lucie, FL | 82.01% | 1,468,525 | 6.62 |

| 8 | Murfreesboro, TN | 134.15% | 2,255,405 | 9.8 |

| 9 | Allen, TX | 92.33% | 1,058,126 | 4.04 |

| 10 | Rio Rancho, NM | 59.18% | 787,323 | 5.6 |

| 11 | Irvine, CA | 120.11% | 3,227,465 | 5.03 |

| 12 | Gilbert, AZ | 165.62% | 2,316,280 | 4.01 |

| 13 | Denton, TX | 99.85% | 1,755,437 | 9.45 |

| 14 | North Las Vegas, NV | 178.16% | 2,433,576 | 4.7 |

| 15 | College Station, TX | 102.11% | 1,241,079 | 8.39 |

| 16 | North Charleston, SC | 49.23% | 972,242 | 4.28 |

| 17 | Killeen, TX | 28.42% | 1,747,841 | 9.42 |

| 18 | Clarksville, TN | 136.87% | 2,326,712 | 11.43 |

| 19 | Nampa, ID | 105.74% | 1,971,325 | 13.66 |

| 20 | Avondale, AZ | 39.61% | 589,599 | 2.73 |

| 21 | Surprise, AZ | 233.64% | 1,475,294 | 6.54 |

| 22 | Sioux Falls, SD | 202.70% | 1,546,150 | 7.65 |

| 23 | Austin, TX | 69.27% | 10,031,773 | 7.95 |

| 24 | Indio, CA | 12.26% | 885,468 | 6.22 |

| 25 | Cape Coral, FL | 95.31% | 1,797,691 | 7.73 |

| 26 | Bend, OR | 65.51% | 1,149,608 | 10.46 |

| 27 | Macon, GA | 38.82% | 1,484,207 | 9.95 |

| 28 | Clovis, CA | 116.48% | 1,177,183 | 6.34 |

| 29 | Fort Worth, TX | 67.00% | 8,708,641 | 6.24 |

| 30 | Lewisville, TX | 54.90% | 2,332,284 | 7.55 |

| 31 | Peoria, AZ | 47.66% | 1,792,192 | 4.32 |

| 32 | Henderson, NV | 60.26% | 3,364,594 | 6.5 |

| 33 | Missouri City, TX | 100.93% | 1,004,484 | 4.37 |

| 35 | Durham, NC | 131.64% | 3,096,678 | 9.24 |

| 36 | Orlando, FL | 79.00% | 8,618,724 | 7.1 |

| 37 | Fontana, CA | 7.67% | 1,387,158 | 3.48 |

| 38 | Raleigh, NC | 65.16% | 4,762,809 | 7.25 |

| 39 | Bryan, TX | 53.65% | 870,957 | 7.13 |

| 40 | Fayetteville, NC | 55.49% | 2,961,411 | 12.1 |

| 41 | Fayetteville, AR | 61.51% | 1,206,041 | 8.47 |

| 42 | Tuscaloosa, AL | 70.00% | 998,626 | 7.46 |

| 43 | Greenville, NC | 22.26% | 1,125,539 | 9.04 |

| 44 | Santa Fe, NM | 35.49% | 1,550,884 | 15.31 |

| 45 | Charlotte, NC | 96.45% | 7,565,519 | 7.18 |

| 46 | Las Cruces, NM | 50.27% | 1,610,950 | 11.31 |

| 47 | Odessa, TX | 46.90% | 1,419,473 | 10.38 |

| 48 | Seattle, WA | 56.36% | 3,752,026 | 3.97 |

| 49 | Santa Clarita, CA | 32.27% | 911,926 | 4.41 |

| 50 | Miami, FL | 106.97% | 8,654,231 | 3.77 |

| 51 | Roseville, CA | 48.86% | 1,764,948 | 6.74 |

| 52 | Folsom, CA | 38.95% | 579,006 | 4.43 |

| 53 | Thornton, CO | 54.89% | 659,480 | 1.93 |

| 54 | Chino, CA | 53.38% | 551,768 | 2.83 |

| 55 | Charleston, SC | 52.78% | 1,710,237 | 6.29 |

| 56 | Jersey City, NJ | 124.01% | 1,049,412 | 1.25 |

| 58 | Kent, WA | 11.30% | 1,416,495 | 3.94 |

| 59 | Broken Arrow, OK | 26.02% | 1,522,717 | 7.19 |

| 60 | Columbia, SC | 51.21% | 3,660,596 | 8.33 |

| 61 | Columbia, MO | 44.45% | 767,197 | 6.09 |

| 62 | O'Fallon, MO | 131.19% | 273,151 | 1.78 |

| 64 | Huntsville, AL | 83.27% | 2,718,071 | 11.2 |

| 65 | Grand Prairie, TX | 37.74% | 1,437,079 | 3.31 |

| 66 | Victorville, CA | 50.56% | 1,624,418 | 8.18 |

| 67 | Palm Bay, FL | 130.10% | 1,007,771 | 7.99 |

| 68 | Nashville, TN | 62.03% | 3,855,372 | 6.57 |

| 69 | Edmond, OK | 129.67% | 2,254,835 | 10.1 |

| 70 | Wilmington, NC | 52.91% | 2,820,076 | 13.07 |

| 71 | Brandon, FL | 21.79% | 831,066 | 4.11 |

| 72 | Rochester, MN | 83.79% | 830,418 | 6.95 |

| 73 | Hillsboro, OR | 118.15% | 983,677 | 4.21 |

| 74 | Madison, WI | 107.71% | 1,464,942 | 4.23 |

| 75 | Sparks, NV | 42.55% | 1,600,846 | 7.86 |

| 76 | Denver, CO | 72.46% | 5,037,957 | 3.45 |

| 77 | Reno, NV | 29.39% | 5,118,698 | 14.32 |

| 78 | Spring Hill, FL | 94.01% | 1,056,466 | 7.5 |

| 80 | Bakersfield, CA | 42.09% | 5,036,656 | 8.82 |

| 81 | Suffolk, VA | 107.72% | 687,613 | 5.29 |

| 82 | Vancouver, WA | 75.05% | 3,127,566 | 8.24 |

| 83 | Visalia, CA | 59.42% | 1,438,984 | 9.23 |

| 84 | Longmont, CO | 35.12% | 1,157,391 | 9.91 |

| 85 | Baytown, TX | 119.29% | 1,593,815 | 13.11 |

| 86 | Asheville, NC | 100.12% | 1,405,289 | 8.51 |

| 87 | Elk Grove, CA | 32.10% | 1,184,895 | 4.32 |

| 88 | Santa Clara, CA | 24.63% | 1,160,934 | 4.23 |

| 89 | Olathe, KS | 71.34% | 1,080,438 | 6.05 |

| 90 | Midland, TX | 64.36% | 1,928,436 | 12.62 |

| 91 | Arlington, VA | 63.17% | 717,825 | 1.16 |

| 92 | Fort Collins, CO | 61.06% | 1,486,804 | 8.05 |

| 93 | Lake Charles, LA | 68.16% | 1,663,671 | 12.99 |

| 94 | West Jordan, UT | 184.33% | 1,107,673 | 3.7 |

| 95 | Spring Valley, NV | 481.02% | 207,541 | 0.65 |

| 96 | San Antonio, TX | 66.86% | 16,778,510 | 9.01 |

| 97 | Washington, DC | 273.94% | 2,010,302 | 2.16 |

| 98 | Beaverton, OR | 23.15% | 1,302,528 | 2.95 |

| 99 | Bellevue, WA | 25.65% | 941,712 | 5.12 |

| 100 | Tallahassee, FL | 38.15% | 2,731,327 | 10.88 |

| 101 | Bellingham, WA | 56.85% | 898,696 | 8.75 |

| 102 | Hoover, AL | 100.18% | 426,700 | 2.96 |

| 103 | Sandy, UT | 27.11% | 638,451 | 3.08 |

| 104 | Brownsville, TX | 58.16% | 957,427 | 5.31 |

| 105 | Gainesville, FL | 55.21% | 1,529,544 | 7.31 |

| 106 | Temecula, CA | 20.99% | 1,226,342 | 7.3 |

| 107 | El Paso, TX | 65.58% | 4,706,312 | 6.11 |

| 108 | San Marcos, CA | 0.00% | 949,839 | 4.17 |

| 110 | Lubbock, TX | 125.78% | 4,430,793 | 16.62 |

| 111 | Highlands Ranch, CO | 70.33% | 351,122 | 1.77 |

| 112 | Lakeland, FL | 81.54% | 2,537,254 | 9.54 |

| 113 | Billings, MT | 84.69% | 2,584,939 | 20.41 |

| 114 | Greeley, CO | 64.68% | 1,038,928 | 7.32 |

| 115 | Colorado Springs, CO | 47.95% | 6,639,052 | 11.04 |

| 116 | Norman, OK | 26.50% | 1,385,237 | 10.71 |

| 117 | Jacksonville, FL | 54.48% | 9,482,299 | 9.54 |

| 118 | Atlanta, GA | 144.25% | 5,545,264 | 4.54 |

| 119 | Overland Park, KS | 84.43% | 1,157,554 | 3.01 |

| 120 | Westminster, CO | 37.76% | 586,380 | 2.64 |

| 121 | Lincoln, NE | 70.45% | 1,877,774 | 6.42 |

| 122 | Greensboro, NC | 63.96% | 3,567,918 | 10.92 |

| 123 | Oklahoma City, OK | 53.27% | 7,092,229 | 8.44 |

| 124 | Richmond, CA | 31.55% | 1,214,450 | 4.07 |

| 125 | Hesperia, CA | 17.39% | 943,809 | 6.82 |

| 126 | West Palm Beach, FL | 49.88% | 3,221,305 | 6.3 |

| 127 | McAllen, TX | 59.35% | 1,113,737 | 4.97 |

| 128 | Spokane Valley, WA | 123.80% | 1,556,075 | 9.4 |

| 129 | Orem, UT | 25.73% | 959,034 | 4.99 |

| 130 | Omaha, NE | 70.33% | 4,881,880 | 7.33 |

| 131 | Chandler, AZ | 99.65% | 2,233,889 | 4.49 |

| 133 | Aurora, CO | 56.67% | 3,035,720 | 4.15 |

| 134 | Miramar, FL | 165.13% | 743,306 | 1.5 |

| 135 | Portland, OR | 155.66% | 4,647,095 | 4.3 |

| 136 | Houston, TX | 42.87% | 27,141,920 | 6.8 |

| 137 | Tampa, FL | 45.70% | 6,704,421 | 6.87 |

| 138 | Waco, TX | 96.21% | 2,144,092 | 10.87 |

| 139 | Minneapolis, MN | 184.89% | 1,820,522 | 2.03 |

| 140 | Irving, TX | 51.13% | 1,951,758 | 6.87 |

| 141 | Moreno Valley, CA | 19.38% | 1,187,427 | 4.28 |

| 142 | Lancaster, CA | 46.50% | 1,346,560 | 8.41 |

| 143 | Palmdale, CA | 8.89% | 969,071 | 5.19 |

| 144 | Lee's Summit, MO | 65.79% | 637,522 | 6.5 |

| 145 | Fort Lauderdale, FL | 57.80% | 2,627,274 | 3.77 |

| 146 | Richmond, VA | 69.25% | 4,002,982 | 5.75 |

| 147 | Cambridge, MA | 0.00% | 88,461 | 0.14 |

| 148 | Scottsdale, AZ | 77.34% | 2,970,404 | 8.2 |

| 149 | Plano, TX | 76.16% | 3,778,674 | 5.51 |

| 150 | Boynton Beach, FL | 8.72% | 922,794 | 3.26 |

| 151 | Boston, MA | 31.02% | 643,067 | 0.7 |

| 152 | Chula Vista, CA | 33.33% | 1,909,396 | 3.64 |

| 153 | Chesapeake, VA | 32.90% | 2,612,225 | 6.51 |

| 154 | Chattanooga, TN | 106.54% | 2,241,916 | 8.11 |

| 156 | Athens, GA | 130.09% | 867,630 | 7.14 |

| 157 | Murrieta, CA | 67.66% | 1,084,310 | 4.86 |

| 158 | Eugene, OR | 40.77% | 1,664,038 | 7.05 |

| 159 | Oakland, CA | 47.12% | 1,599,150 | 2.44 |

| 160 | Everett, WA | 16.16% | 1,157,999 | 4.52 |

| 161 | Yakima, WA | 44.06% | 1,035,179 | 7.97 |

| 162 | Lake Forest, CA | 25.84% | 886,628 | 4.03 |

| 163 | Oxnard, CA | 21.78% | 1,494,047 | 5.27 |

| 164 | Elgin, IL | 19.95% | 600,925 | 2.39 |

| 165 | Redondo Beach, CA | 0.00% | 279,392 | 0.75 |

| 166 | Arvada, CO | 98.55% | 932,279 | 3.53 |

| 167 | Albany, NY | 83.01% | 647,586 | 2.87 |

| 168 | New Haven, CT | 465.75% | 435,139 | 2.44 |

| 169 | Santa Ana, CA | 0.00% | 1,243,539 | 1.58 |

| 171 | Amarillo, TX | 45.51% | 2,388,926 | 11.22 |

| 172 | West Valley City, UT | 87.58% | 1,316,380 | 4.04 |

| 173 | Mesa, AZ | 48.10% | 4,970,989 | 5.8 |

| 174 | Fremont, CA | 18.59% | 1,093,159 | 3.51 |

| 175 | Quincy, MA | 201.90% | 442,463 | 2.08 |

| 176 | Ontario, CA | 28.28% | 819,578 | 2.41 |

| 177 | Merced, CA | 0.00% | 590,119 | 6.01 |

| 178 | Lynchburg, VA | 37.57% | 721,960 | 7.79 |

| 180 | Salt Lake City, UT | 47.70% | 2,647,796 | 3.47 |

| 181 | Carrollton, TX | 27.29% | 2,125,376 | 4.75 |

| 182 | Tempe, AZ | 30.52% | 2,027,780 | 4.19 |

| 183 | Joliet, IL | 97.41% | 777,858 | 3.89 |

| 184 | Tacoma, WA | 62.11% | 2,595,618 | 4.38 |

| 185 | Lawrence, KS | 38.42% | 687,428 | 7.82 |

| 186 | Worcester, MA | 240.53% | 784,471 | 3.29 |

| 187 | Sacramento, CA | 39.58% | 6,058,612 | 4.99 |

| 188 | Phoenix, AZ | 78.80% | 10,744,884 | 5.48 |

| 189 | Newark, NJ | 163.20% | 736,238 | 0.92 |

| 190 | Simi Valley, CA | 37.49% | 835,557 | 6.31 |

| 191 | Lafayette, LA | 55.69% | 2,375,805 | 13.16 |

| 192 | Columbus, OH | 47.29% | 5,284,984 | 4.44 |

| 193 | Salem, OR | 68.03% | 2,148,342 | 8.27 |

| 194 | Alexandria, VA | 65.54% | 1,830,831 | 2.93 |

| 195 | Little Rock, AR | 64.55% | 3,050,508 | 12.77 |

| 196 | Sandy Springs, GA | 91.04% | 696,654 | 2.99 |

| 197 | Corpus Christi, TX | 33.73% | 3,748,605 | 12.31 |

| 198 | Mount Vernon, NY | 202.79% | 412,683 | 0.65 |

| 199 | Las Vegas, NV | 40.47% | 13,814,925 | 7.54 |

| 200 | Silver Spring, MD | 0.00% | 715,120 | 1.18 |

| 201 | Pompano Beach, FL | 27.95% | 2,097,490 | 5.26 |

| 202 | Stamford, CT | 57.37% | 1,031,069 | 6.03 |

| 203 | Vacaville, CA | 57.91% | 996,872 | 7.72 |

| 204 | Lexington, KY | 74.05% | 2,484,553 | 8.01 |

| 205 | San Francisco, CA | 20.72% | 2,210,592 | 2.1 |

| 206 | Danbury, CT | 72.43% | 499,608 | 5.48 |

| 207 | Savannah, GA | 75.83% | 2,013,442 | 8.25 |

| 208 | Albuquerque, NM | 33.97% | 5,348,996 | 7.74 |

| 209 | Somerville, MA | 44.09% | 490,633 | 0.68 |

| 210 | Fort Wayne, IN | 97.56% | 2,206,202 | 6.97 |

| 211 | Columbia, MD | 106.59% | 680,578 | 3.75 |

| 212 | Fresno, CA | 38.51% | 4,853,329 | 7.05 |

| 213 | Boca Raton, FL | 37.62% | 1,563,348 | 4.63 |

| 214 | Santa Rosa, CA | 20.12% | 2,025,565 | 8.05 |

| 215 | Brooklyn Park, MN | 63.35% | 485,070 | 2.88 |

| 216 | Mountain View, CA | 0.00% | 459,637 | 2.68 |

| 218 | Union City, CA | 0.00% | 161,093 | 0.65 |

| 219 | Springfield, MO | 50.44% | 2,571,999 | 10.61 |

| 220 | Berkeley, CA | 5.25% | 436,977 | 1.58 |

| 221 | Bloomington, IN | 49.53% | 644,796 | 5.22 |

| 222 | Dallas, TX | 41.45% | 10,154,435 | 5.15 |

| 223 | Providence, RI | 202.92% | 649,129 | 1.62 |

| 224 | South Gate, CA | 0.00% | 538,168 | 0.81 |

| 225 | Los Angeles, CA | 35.26% | 6,679,824 | 1.83 |

| 226 | San Jose, CA | 40.34% | 4,526,878 | 3.93 |

| 227 | Boulder, CO | 13.48% | 744,606 | 6.11 |

| 228 | Philadelphia, PA | 84.43% | 6,318,372 | 3.24 |

| 229 | Federal Way, WA | 104.68% | 948,008 | 5.08 |

| 230 | Upland, CA | 0.00% | 748,724 | 2.31 |

| 231 | Lynn, MA | 107.01% | 284,726 | 1.71 |

| 232 | Kansas City, MO | 60.63% | 2,861,309 | 3.7 |

| 233 | Toms River, NJ | 48.59% | 720,807 | 3.97 |

| 234 | San Diego, CA | 42.69% | 6,620,025 | 4.09 |

| 235 | Apple Valley, CA | 26.55% | 390,120 | 3.96 |

| 236 | Tracy, CA | 10.12% | 575,979 | 6.05 |

| 237 | Mission Viejo, CA | 18.29% | 282,197 | 0.84 |

| 238 | High Point, NC | 59.48% | 1,157,903 | 6.77 |

| 239 | Columbus, GA | 62.07% | 2,463,459 | 11.2 |

| 240 | Union City, NJ | 0.00% | 97,599 | 0.14 |

| 241 | Arlington, TX | 36.48% | 3,777,892 | 5.78 |

| 242 | Rancho Cucamonga, CA | 35.69% | 1,622,245 | 4.51 |

| 243 | Brockton, MA | 29.59% | 330,992 | 2.9 |

| 244 | Davie, FL | 22.38% | 1,468,218 | 3.4 |

| 245 | Richardson, TX | 26.27% | 576,644 | 2.29 |

| 246 | Sunnyvale, CA | 27.54% | 868,505 | 2.44 |

| 248 | Santa Monica, CA | 42.33% | 217,289 | 0.76 |

| 249 | Stockton, CA | 8.41% | 2,424,120 | 6.76 |

| 250 | Waukesha, WI | 159.69% | 666,132 | 5.93 |

| 251 | Norwalk, CT | 64.29% | 659,416 | 5.4 |

| 252 | Daly City, CA | 20.78% | 524,088 | 1.03 |

| 253 | Anaheim, CA | 17.68% | 1,578,273 | 1.51 |

| 254 | Antioch, CA | 39.75% | 655,304 | 3.88 |

| 255 | Carlsbad, CA | 62.68% | 773,669 | 4.5 |

| 256 | Paterson, NJ | 42.53% | 338,018 | 0.78 |

| 257 | St. Paul, MN | 285.54% | 1,712,456 | 3.27 |

| 258 | Dearborn, MI | 5.59% | 277,971 | 1.02 |

| 259 | Lowell, MA | 0.00% | 75,565 | 0.49 |

| 260 | Pleasanton, CA | 18.23% | 532,780 | 3.74 |

| 262 | Turlock, CA | 30.52% | 883,851 | 10.29 |

| 263 | Kenosha, WI | 101.78% | 764,914 | 6.27 |

| 264 | Gulfport, MS | 57.73% | 1,345,953 | 13.29 |

| 265 | Lakewood, CO | 66.64% | 1,472,546 | 3.42 |

| 266 | Modesto, CA | 14.51% | 2,200,604 | 6.43 |

| 267 | Louisville, KY | 80.01% | 6,270,806 | 7.58 |

| 268 | Mesquite, TX | 29.63% | 1,418,997 | 3.39 |

| 269 | Hemet, CA | 5.63% | 873,752 | 5.12 |

| 270 | Carson, CA | 131.70% | 521,347 | 1.08 |

| 271 | Spokane, WA | 56.90% | 2,883,514 | 7.26 |

| 273 | Vista, CA | 17.85% | 1,111,140 | 4.33 |

| 274 | Longview, TX | 46.88% | 1,669,932 | 15.97 |

| 275 | Virginia Beach, VA | 38.33% | 5,974,594 | 10.7 |

| 276 | Plymouth, MN | 79.36% | 604,802 | 3.22 |

| 277 | Naperville, IL | 113.55% | 922,002 | 2.81 |

| 278 | Bolingbrook, IL | 43.43% | 635,660 | 3.16 |

| 279 | Gresham, OR | 12.57% | 657,223 | 2.9 |

| 282 | Waterbury, CT | 0.00% | 312,377 | 2.12 |

| 283 | Pawtucket, RI | 22.78% | 412,001 | 1.92 |

| 284 | Bloomington, MN | 205.70% | 725,323 | 4.42 |

| 285 | Plantation, FL | 58.75% | 648,497 | 1.52 |

| 286 | Anchorage, AK | 24.19% | 1,436,698 | 6.44 |

| 287 | Miami Gardens, FL | 109.00% | 456,467 | 1.09 |

| 289 | Wilmington, DE | 32.38% | 446,416 | 2.64 |

| 290 | Coral Springs, FL | 14.80% | 552,519 | 5.09 |

| 291 | Wyoming, MI | 7.36% | 507,062 | 2.29 |

| 292 | Lawrence, MA | 413.79% | 170,736 | 1.15 |

| 293 | St. Petersburg, FL | 107.95% | 2,489,148 | 5.9 |

| 294 | Deerfield Beach, FL | 36.53% | 838,014 | 3.36 |

| 295 | Aurora, IL | 23.30% | 768,996 | 2.49 |

| 296 | Hialeah, FL | 87.81% | 1,130,425 | 2.13 |

| 297 | Peoria, IL | 96.15% | 1,294,229 | 8.76 |

| 298 | Oceanside, CA | 0.00% | 830,807 | 3.12 |

| 299 | Escondido, CA | 51.88% | 1,164,144 | 4.66 |

| 300 | Augusta, GA | 58.28% | 2,363,463 | 9.35 |

| 301 | Chino Hills, CA | 81.05% | 218,042 | 2.67 |

| 302 | Ogden, UT | 47.61% | 1,624,686 | 7.03 |

| 303 | Torrance, CA | 10.49% | 1,818,011 | 3.24 |

| 304 | Hayward, CA | 18.56% | 1,115,010 | 2.72 |

| 305 | Lynwood, CA | 0.00% | 97,828 | 0.2 |

| 306 | Lawton, OK | 31.57% | 1,084,315 | 12.55 |

| 307 | Burbank, CA | 45.29% | 548,516 | 1.61 |

| 308 | Farmington Hills, MI | 69.03% | 482,943 | 2.18 |

| 309 | Chicago, IL | 76.95% | 11,581,226 | 3.37 |

| 310 | Tucson, AZ | 47.09% | 6,696,706 | 8.55 |

| 311 | Pasadena, CA | 3.32% | 1,162,575 | 2.88 |

| 314 | Wichita, KS | 57.48% | 3,016,086 | 6.74 |

| 315 | Fort Smith, AR | 34.34% | 796,078 | 7.56 |

| 316 | Troy, MI | 45.84% | 932,812 | 4.3 |

| 317 | Glendale, AZ | 21.35% | 2,295,641 | 2.81 |

| 318 | Cicero, IL | 45.14% | 486,031 | 0.95 |

| 319 | Scranton, PA | 124.22% | 386,615 | 3.35 |

| 320 | Vallejo, CA | 12.10% | 865,841 | 5.13 |

| 321 | Manchester, NH | 69.88% | 516,753 | 3.58 |

| 322 | Cedar Rapids, IA | 190.52% | 948,755 | 5.49 |

| 323 | Ventura, CA | 13.29% | 1,321,180 | 7.56 |

| 324 | Clifton, NJ | 65.84% | 758,315 | 1.3 |

| 325 | Long Beach, CA | 4.85% | 2,182,103 | 2.06 |

| 326 | Gastonia, NC | 155.21% | 942,444 | 8.84 |

| 327 | Alhambra, CA | 106.10% | 332,805 | 0.88 |

| 328 | Centennial, CO | 41.94% | 791,669 | 2.43 |

| 329 | South Bend, IN | 69.04% | 925,841 | 4.5 |

| 330 | Corona, CA | 90.97% | 1,481,934 | 4.08 |

| 331 | Norfolk, VA | 34.61% | 1,971,213 | 5.1 |

| 332 | Knoxville, TN | 115.03% | 4,382,555 | 9.73 |

| 333 | Costa Mesa, CA | 2.23% | 1,287,018 | 3.64 |

| 334 | Provo, UT | 17.17% | 774,260 | 4.8 |

| 335 | Glendale, CA | 112.24% | 668,624 | 1.9 |

| 337 | New Britain, CT | 2743.99% | 176,697 | 1.67 |

| 338 | Appleton, WI | 104.24% | 1,487,776 | 7.93 |

| 339 | Sterling Heights, MI | 54.58% | 720,431 | 2.21 |

| 340 | Davenport, IA | 87.64% | 1,225,767 | 8.12 |

| 341 | Hawthorne, CA | 74.26% | 647,486 | 1.25 |

| 342 | Buena Park, CA | 14.66% | 367,805 | 1.11 |

| 343 | Bethlehem, PA | 65.27% | 401,039 | 2.04 |

| 344 | Baton Rouge, LA | 60.19% | 4,507,502 | 11.04 |

| 345 | Melbourne, FL | 37.44% | 1,628,120 | 6.58 |

| 346 | San Leandro, CA | 8.27% | 919,540 | 2.8 |

| 347 | Fairfield, CA | 16.87% | 1,303,373 | 8.23 |

| 348 | Concord, CA | 0.00% | 1,001,446 | 4.3 |

| 349 | Hartford, CT | 0.00% | 180,664 | 0.85 |

| 351 | Rockford, IL | 52.69% | 928,613 | 4.04 |

| 352 | Huntington Beach, CA | 1.90% | 1,106,354 | 2.5 |

| 353 | Indianapolis, IN | 45.78% | 7,822,425 | 6.87 |

| 354 | Santa Barbara, CA | 0.00% | 663,105 | 4.08 |

| 355 | Roanoke, VA | 41.99% | 1,362,855 | 7.06 |

| 356 | Rochester Hills, MI | 37.02% | 565,533 | 4.29 |

| 357 | Deltona, FL | 176.98% | 348,839 | 2.97 |

| 358 | Westminster, CA | 4.35% | 713,493 | 1.63 |

| 359 | Hampton, VA | 47.35% | 833,591 | 3.97 |

| 360 | Des Moines, IA | 111.63% | 1,510,823 | 4.87 |

| 361 | Clearwater, FL | 34.25% | 1,866,034 | 4.84 |

| 362 | Napa, CA | 10.30% | 956,262 | 11.26 |

| 363 | Evanston, IL | 128.27% | 239,472 | 0.71 |

| 364 | Grand Rapids, MI | 209.35% | 1,584,165 | 3.67 |

| 365 | Thousand Oaks, CA | 113.85% | 321,846 | 2.79 |

| 366 | Ann Arbor, MI | 4.63% | 809,815 | 4.07 |

| 367 | Elizabeth, NJ | 33.14% | 297,119 | 0.79 |

| 368 | Santa Maria, CA | 28.92% | 1,465,632 | 10.71 |

| 369 | Beaumont, TX | 47.02% | 1,524,968 | 13.65 |

| 370 | Newport News, VA | 46.49% | 1,550,531 | 6.34 |

| 372 | Tulsa, OK | 42.16% | 5,147,146 | 9.06 |

| 373 | San Mateo, CA | 33.24% | 477,181 | 2.43 |

| 374 | Largo, FL | 45.04% | 1,548,907 | 5.4 |

| 375 | Fall River, MA | 79.63% | 315,291 | 3.79 |

| 376 | Redwood City, CA | 11.04% | 832,904 | 5.12 |

| 377 | Westland, MI | 19.15% | 601,208 | 2.47 |

| 379 | Rochester, NY | 76.07% | 1,684,458 | 3.46 |

| 380 | Yonkers, NY | 81.52% | 934,276 | 1.97 |

| 382 | Evansville, IN | 51.61% | 1,276,576 | 7.95 |

| 383 | Waukegan, IL | 40.76% | 341,088 | 2.09 |

| 384 | New Rochelle, NY | 240.15% | 552,822 | 2.09 |

| 385 | New Bedford, MA | 267.93% | 651,799 | 4.49 |

| 386 | Newport Beach, CA | 0.00% | 237,004 | 1.03 |

| 387 | Southfield, MI | 29.89% | 765,350 | 2.71 |

| 389 | Roswell, GA | 43.82% | 708,502 | 3.39 |

| 390 | Arlington Heights, IL | 49.57% | 562,157 | 1.7 |

| 391 | Muncie, IN | 50.53% | 673,551 | 7.77 |

| 392 | Independence, MO | 26.97% | 920,719 | 5.88 |

| 394 | Citrus Heights, CA | 0.00% | 355,575 | 1.27 |

| 395 | Fullerton, CA | 14.51% | 781,276 | 1.44 |

| 397 | Kansas City, KS | 31.90% | 727,799 | 2.82 |

| 398 | Rialto, CA | 56.53% | 890,993 | 2.83 |

| 399 | Lansing, MI | 106.04% | 1,354,360 | 6.54 |

| 400 | Passaic, NJ | 80.70% | 148,028 | 0.43 |

| 401 | Bridgeport, CT | 65.17% | 492,552 | 2.02 |

| 402 | Metairie, LA | 55.41% | 1,101,838 | 3.62 |

| 404 | Allentown, PA | 146.01% | 976,626 | 3.46 |

| 405 | Pembroke Pines, FL | 63.09% | 979,881 | 2.38 |

| 406 | St. Cloud, MN | 0.00% | 117,511 | 1.36 |

| 407 | Hollywood, FL | 60.02% | 1,059,368 | 2.18 |

| 408 | Norwalk, CA | 55.22% | 612,284 | 1.32 |

| 409 | Orange, CA | 10.85% | 1,171,241 | 2.32 |

| 411 | Pittsburgh, PA | 43.87% | 3,200,226 | 3.55 |

| 413 | Whittier, CA | 23.65% | 700,797 | 1.28 |

| 414 | Syracuse, NY | 140.58% | 798,327 | 3.22 |

| 415 | Trenton, NJ | 96.88% | 503,403 | 2.08 |

| 416 | Jackson, MS | 37.32% | 1,359,783 | 6.58 |

| 418 | Warwick, RI | 134.06% | 281,437 | 1.47 |

| 419 | Inglewood, CA | 50.90% | 537,338 | 1.05 |

| 421 | Sunrise, FL | 0.00% | 277,223 | 1.44 |

| 422 | Nashua, NH | 88.92% | 1,178,043 | 9.37 |

| 423 | Salinas, CA | 33.41% | 1,116,562 | 5.91 |

| 424 | Riverside, CA | 12.21% | 3,581,638 | 5.7 |

| 425 | Weston, FL | 106.28% | 363,642 | 3.11 |

| 427 | Racine, WI | 37.23% | 363,573 | 3.01 |

| 428 | Portsmouth, VA | 45.97% | 712,975 | 3.37 |

| 429 | Milwaukee, WI | 88.81% | 3,078,753 | 3.74 |

| 430 | Schaumburg, IL | 36.06% | 634,070 | 2.36 |

| 431 | El Monte, CA | 26.16% | 586,193 | 1.64 |

| 432 | Hammond, IN | 67.77% | 392,799 | 1.92 |

| 433 | Pomona, CA | 27.40% | 876,707 | 2.31 |

| 434 | Mobile, AL | 37.50% | 2,895,476 | 10.87 |

| 435 | Baldwin Park, CA | 0.00% | 121,290 | 0.45 |

| 437 | Livonia, MI | 51.42% | 877,482 | 2.92 |

| 438 | Lorain, OH | 134.07% | 293,316 | 4.05 |

| 439 | Newton, MA | 165.27% | 316,725 | 1.1 |

| 440 | El Cajon, CA | 20.62% | 1,070,375 | 3.21 |

| 441 | Cranston, RI | 465.46% | 320,552 | 1.2 |

| 443 | Reading, PA | 193.51% | 669,484 | 3.15 |

| 444 | Kalamazoo, MI | 81.69% | 693,216 | 4.16 |

| 445 | Garland, TX | 59.50% | 2,172,445 | 3.9 |

| 446 | Baltimore, MD | 58.85% | 4,448,150 | 3.76 |

| 447 | Buffalo, NY | 138.23% | 863,643 | 1.61 |

| 448 | San Bernardino, CA | 21.10% | 1,460,270 | 3.35 |

| 449 | Parma, OH | 189.79% | 358,029 | 1.57 |

| 450 | Alameda, CA | 13.03% | 667,215 | 1.92 |

| 452 | Springfield, MA | 152.25% | 451,851 | 2.55 |

| 453 | Birmingham, AL | 42.39% | 3,663,534 | 7.33 |

| 454 | Canton, OH | 25.47% | 737,692 | 4.32 |

| 455 | Warren, MI | 28.21% | 892,862 | 2.18 |

| 457 | Memphis, TN | 31.21% | 6,159,015 | 8.13 |

| 458 | Livermore, CA | 14.39% | 778,150 | 7.58 |

| 459 | Compton, CA | 391.62% | 277,451 | 0.44 |

| 460 | Palatine, IL | 18.41% | 452,003 | 2.15 |

| 461 | Akron, OH | 50.74% | 1,728,080 | 4.89 |

| 462 | Kendall, FL | 0.00% | 72,165 | 0.48 |

| 463 | Miami Beach, FL | 22.85% | 109,404 | 0.77 |

| 464 | Cincinnati, OH | 44.72% | 3,671,755 | 3.96 |

| 465 | Pasadena, TX | 29.04% | 2,132,132 | 6.45 |

| 467 | West Covina, CA | 20.20% | 330,850 | 0.97 |

| 468 | Paradise, NV | 0.00% | 103,487 | 0.71 |

| 470 | Honolulu, HI | 120.06% | 1,215,574 | 3.21 |

| 472 | Cleveland, OH | 37.59% | 1,730,395 | 2.27 |

| 473 | Toledo, OH | 97.12% | 1,773,711 | 4.49 |

| 474 | Bellflower, CA | 11.18% | 164,701 | 0.31 |

| 476 | Downey, CA | 0.00% | 306,696 | 0.69 |

| 477 | Redlands, CA | 48.61% | 767,636 | 5.5 |

| 478 | Garden Grove, CA | 338.02% | 281,269 | 0.44 |

| 479 | New Orleans, LA | 92.84% | 2,510,285 | 4.56 |

| 480 | Lakewood, CA | 0.00% | 142,735 | 0.31 |

| 481 | Dale City, VA | 313.85% | 129,902 | 1.03 |

| 482 | Cheektowaga, NY | 0.00% | 278,728 | 1.61 |

| 484 | Kenner, LA | 159.36% | 632,282 | 4.24 |

| 485 | Dayton, OH | 31.69% | 1,523,392 | 3.65 |

| 486 | Detroit, MI | 51.30% | 1,015,356 | 1.16 |

| 487 | Tustin, CA | 72.71% | 530,089 | 1.45 |

| 488 | Gary, IN | 20.50% | 116,170 | 1.18 |

| 489 | Flint, MI | 85.31% | 949,048 | 4.79 |

Despite the challenges facing the housing market, there are encouraging signs of progress and adaptation. Regions like the Sunbelt and Mountain West are actively building to meet demand, with cities in Texas, Florida and Utah leading the way in new home construction. Innovations in construction technology and strategic zoning changes in some cities are also paving the path for more diverse housing options, including much-needed middle housing. While obstacles such as rising costs and supply chain delays persist, the commitment to expanding inventory remains strong. As markets adjust, these efforts are gradually creating a more balanced housing landscape, bringing us closer to meeting the nation’s housing needs.

Check out how cities across the U.S. fared in terms of housing inventory evolution alongside some other metrics that help shape housing demand:

What the experts are saying

To get additional insights into the evolution of the housing stock, we've turned to expert opinions below:

Michael L. Garrison, Professor at the University of Texas at Austin, School of Architecture

1. Which type of housing is best suited to address the housing demand?

The best type of housing to meet demand would be medium-density multifamily attached housing with about 30-32 units per acre and built in urban locations where demand is typically high.

2. Which areas of the U.S. are best positioned to meet the housing demand and what are the reasons behind it?

The best areas of the country to meet housing demand are growing cities featuring high-tech jobs. Moreover, as we enter the AI era, you’re also likely to green cities where utilities have a high rate of non-carbon emissions and manage the water supply and waste are also in a great position to respond to the demand for housing.

3. How do you see the housing supply evolving in the future?

The US does not have enough available housing units and we must increase supply. Some ways to increase supply may include utility and tax breaks for affordable green housing. Limiting outside land trusts and hedge funds from using leveraged assets and rental housing as an investment tool rather than a homebuyer meeting family housing needs. Another solution to boost housing stock is to have reduced down payment requirements for qualified first-time home buyers. Zoning benefits for developers in exchange for green and affordable housing can also serve this purpose. Moreover, supporting community based-land trusts and creating a housing finance housing similar to the GI bill in exchange for community or military service can help create more homes. Building differently can also support this goal – more prefabrication and off-site partial construction by upgrading building codes. New DOE and EPA programs that support and require lowering the embodied energy carbon emissions equivalents for home building materials could also contribute to seeing more new homes hitting the market.

Anthony W. Orlando Associate Professor, Finance, Real Estate, and Law, College of Business Administration at California State Polytechnic University-Pomona

1. What types of homes are most effective in meeting current housing demand, and are there notable regional differences in how markets are adapting?

Our national housing shortage is so severe at this point that we need to build all sorts of housing types. Of course, different types will make sense in different neighborhoods. Suburban neighborhoods, with only single-family houses, often worry that new housing will take the form of tall buildings, but that's rarely the case. Developers don't want to spend more on construction than they have to, and they know that tall buildings cost more per square foot than short buildings. They go taller when the land is more expensive, requiring more revenue from more tenants to cover their costs. Increasingly, this is the strategy we need to accommodate the demand for new housing from so many residents, especially in large, growing cities. Over the decades, we have built on most of the land, sprawling out into the suburbs as far as we could until we couldn't sprawl anymore. Now, we're turning back to the core, where our only option is to squeeze tall apartment buildings into difficult locations. In these cities, where wages and productivity and opportunities are highest, we need multifamily housing the most, not the single-family detached homes that we relied upon throughout the twentieth century.

2. What solutions have proven most effective in addressing the housing crisis?

Construction. Market-rate and low-income. Luxury and government-subsidies. In the past few years, economists have compiled a wealth of evidence showing that construction of new apartment buildings leads to lower rents throughout the surrounding neighborhood — and even across the metropolitan area — for residents across the income distribution.

3. In what ways does the current housing supply influence home prices?

Supply restrictions are the leading cause of high prices. Demand is increasing faster than supply, as it has become increasingly difficult to build new housing over the years. This is especially true in high-wage, high-productivity cities — and within those cities, especially in the high-opportunity neighborhoods where children have the best chances of climbing the socioeconomic ladder. If we want to overcome the lingering legacy of segregation, concentrated poverty, and inequality, we need to welcome new residents into these neighborhoods at the same time that we invest in transforming the rest of our urban landscape into high-opportunity neighborhoods as well.

Doug Ressler, Business Intelligence Manager at Yardi Matrix

1. How are housing inventories changing in response to demand?

Beyond inventory changes caused by housing market fluctuations, with homes staying listed longer, availability is improving thanks to stock expansions. Migration hotspots like cities in Texas and Arizona stand out as areas where housing inventories are rapidly increasing. Single-family home expansion is being driven by heightened demand from people seeking more space in their housing choices. At the same time, apartments have accounted for a significant share of new development activity, while self storage is also stepping up to help address living space and affordability challenges.

2. What’s the state of 'missing middle' housing?

The shortage of middle housing—often called “Missing Middle Housing”—remains a major challenge for many communities, even as housing inventories improve in some areas. Migration hotspots like cities in Texas and Arizona are seeing their housing stock grow, driven by strong demand for single-family homes and apartments. However, there’s still a significant gap in housing options like duplexes, triplexes, and townhomes, which could make a big difference in affordability and accessibility.

Several factors contribute to the shortage of middle housing. Zoning laws often favor single-family homes or large apartment buildings, leaving little room for “in-between” options. Rising construction costs for materials and labor make building middle-income housing less profitable for developers, while limited land availability in urban areas adds to the challenge. Even when land is available, it’s often expensive, and developers frequently struggle to secure financing for middle housing projects because they’re seen as less lucrative than luxury developments.

The impact of this shortage is widespread. Middle-income families, who earn too much to qualify for low-income housing but not enough to afford high-end options, are particularly affected. Young professionals, often looking for affordable housing near city centers where they work, find themselves priced out. Older adults seeking to downsize from larger homes also face challenges in finding suitable options in their communities.

The ripple effects of the middle housing shortage extend beyond individuals. Rising housing costs make it harder for middle-income households to find affordable options, while limited choices restrict economic mobility, making it difficult for people to move to areas with better job opportunities. Community stability also takes a hit, as residents are forced to relocate farther from their jobs and social networks, disrupting neighborhoods.

While single family homes and apartments dominate new developments, there’s still much work to be done to address the missing middle. Self storage is helping in small ways, giving people more flexibility to make the most of their living spaces, but it’s not a long-term fix. To truly address the issue, we need a shift in how housing is planned and built. Reviving the “Missing Middle” means rethinking zoning laws, offering financial incentives for developers, and exploring creative solutions like converting offices into housing. These changes can make better use of existing spaces while fostering communities where people of all income levels can thrive.

Methodology

This analysis was done by StorageCafe, an online platform that provides storage unit listings across the nation.

To come up with this report, we analyzed 489 cities with a population of over 55K people, and we ranked them on their housing inventory change performance from 2005 to 2023, according to the latest U.S. Census data. Housing types include single family, multifamily, middle housing, mobile home, boat, RV and van (if used as a main residence) inventory changes . Data on housing stock changes came from the 1-year estimates from the American Community Survey, except for 2020 data, which reflects data provided by the 5-year American Community Survey on housing construction and inventory growth.

For the purpose of this report, a single family home is a detached housing unit. Based on the housing types listed by the U.S. Census, the middle housing classification in our study includes one-unit detached homes and structures with two or more units in buildings up to 19 units. As for multifamily housing, this type of housing includes units in buildings with a minimum of 20 units in our report.

Mobile homes include towable recreational vehicles, such as travel trailers or fifth-wheel trailers that aren’t used for business or extra sleeping space or are for sale. This category comprises both occupied and vacant mobile homes to which no permanent rooms have been added.

The boat, RV, van and more category includes types of housing units used as living quarters that weren’t included in the previous groups. Houseboats, self-propelled recreational vehicles, motor homes, railroad cars, campers and vans are examples listed in this group. As for recreational vehicles — boats, vans, tents, railroad cars and the like — fall under this umbrella only if they’re used as a current residence.

For the single family, multifamily and middle housing categories, we've looked at how cities performed based on population size as listed in the graphs of their respective sections. We classified them as big cities (250K+), mid-sized cities (100K-249.9K) and small cities (>100K).

We’ve also included additional data on the distribution of housing per capita, home prices and rents that came from the U.S. Census. Moreover, for employment stats, we turned to the U.S. Bureau of Labor Statistics.

Data on self storage comes from Yardi Matrix, StorageCafe’s sister division and a business development and asset management tool for brokers, sponsors, banks and equity sources underwriting investments in the multifamily, office, industrial and self storage sectors.

Fair use and distribution

This study serves as a resource for the general public on issues of common interest and should not be regarded as investment advice. The data is true to the best of our knowledge but may change if amendments to it are made. We agree to the distribution of this content but we do require a mention in return for attribution purposes.

Drive-Up Storage Units: Pros, Cons and When They’re Worth It

A drive-up storage unit is a ground-level space with an exterior roll-up door, a lot like a detached garage. Units are usually arranged in rows with wide, paved aisles between them, so you can pull a car, van, or moving truck directly up to your door during access hours. The key feature is the access, and it comes in a few forms:

2026’s Best Cities for Roommates: Irvine, CA And Atlanta, GA, Lead In Shared Living Gains

Americans sharing a two-bedroom apartment instead of renting a one-bedroom alone can save, on average, about $6,700 per year. In some of the country’s most expensive cities, including Irvine, California, or Jersey City, New Jersey, the savings gap widens to around $13,000. For a growing share of renters, living with roommates is less of a lifestyle arrangement and more a conscious financial strategy.

How to Organize Your Kitchen Drawers: Smart, Practical Ideas That Make a Real Difference

The best way to organize your kitchen drawers boils down to a few core principles: give each drawer a specific role, store items close to where you use them, and choose organizers only after you’ve decluttered. Most kitchen drawers aren’t cluttered because of a genuine lack of space but because no one decided what belongs where. Fix that first, and the rest becomes much easier.

The Ultimate New Home Checklist: 20 Essential Boxes to Tick

Moving into a new home is thrilling and stressful in equal measure. While you’re busy planning the big-ticket items like furniture and appliances, it’s easy to forget a handful of smaller essentials that you’ll suddenly need right before or just after the move. That’s exactly why a good new home checklist is worth keeping close. To make your move as smooth as possible, we’ve pulled together the ultimate list of basic items and setup tasks that cover everything your new place needs. First-time buyer or seasoned mover, this guide will help you settle in safely and comfortably, without those maddening last-minute runs to the store.

How to Store Trading Cards (Without Losing Your Grails)

The right way to store trading cards is a layered system, like gearing up for a boss, but the boss is time and physics. For this quest, you’ll need penny sleeves to protect surfaces, rigid holders to protect structure, archival boxes or binders to provide organization and access, and climate control — around 65–72°F and 40–50% humidity — to protect everything else. That combination keeps cards mint whether you have fifty or five thousand of them.

How to Store and Winterize Your First RV: A Complete Beginner’s Guide

Storing and winterizing an RV properly is the difference between an RV that holds its value and stays reliable for years and one that greets you in spring with cracked pipes and a dead battery. This guide covers where to store your RV between trips, how to winterize it before the first hard freeze, and what to check before your first trip of the season along with the basics of choosing and buying your first unit.

Do You Need Climate-Controlled Storage? A Practical Guide to Making the Right Call

Most people need climate-controlled storage for one of the following reasons: they’re storing valuable items that can be damaged by unchecked temperature or humidity, they live in a climate with extreme weather conditions or they plan to store their belongings for an extended period.

StorageCafe Now Has a Dedicated Storage Unit Price Guide

If you’ve ever tried to figure out whether a storage quote was fair, you know the problem. You see a monthly rate, but you have no way to tell whether it’s a deal, a premium-level price, or right in line with the market — and pricing tools that give you real context are surprisingly hard to find.

StorageCafe’s Industry Trends Page: A Sharper Look at the Market

When it comes to self storage, the hard part is finding data that’s both current and retrospective, both granular and sweeping, but also — and most importantly — trustworthy enough to act on. After all, national averages age quickly, and the numbers that move decisions live at the metro and submarket level. Regularly refreshed and highly authoritative, StorageCafe’s Self Storage Industry Trends page exists to close that very gap for professionals in the self storage sector, as well as real estate reporters and journalists. It brings live, nationwide market data into one place and breaks it down city by city, drawing on the same intelligence the professional side of the business relies on. Here’s what it covers and why it’s worth keeping open in a tab.